Healthcare costs are rising faster than inflation in most Tier-1 countries, making health insurance not just a safety net but a financial necessity. In 2026, choosing the right health insurance plan requires careful evaluation of coverage, premiums, deductibles, provider networks, and long-term value.

Whether you are purchasing health insurance for the first time, switching providers, or reviewing your existing plan, this comprehensive guide will help you make a smart, future-proof decision.

Why Choosing the Right Health Insurance Plan Matters More in 2026

In countries like the United States, a single emergency hospital visit can cost anywhere between $5,000 and $50,000 or more. Without adequate coverage, medical bills can quickly lead to long-term financial stress or debt.

- Higher premiums due to medical inflation

- Increased use of AI-based diagnostics and treatments

- Greater focus on preventive care and mental health

- Stricter insurance underwriting policies

Choosing the wrong plan may result in high out-of-pocket costs, limited hospital access, or denied claims.

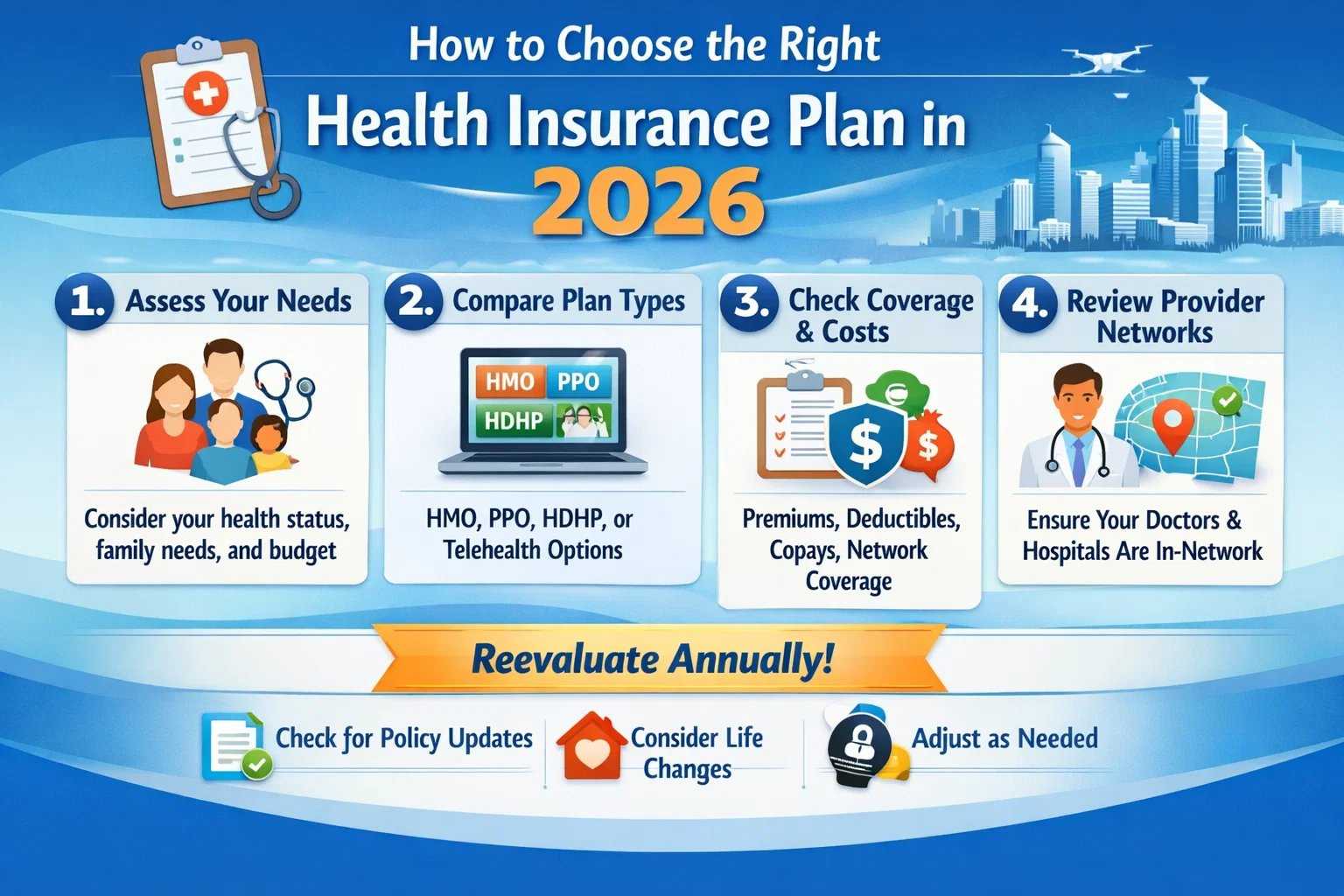

Step 1: Assess Your Personal and Family Healthcare Needs

Before comparing health insurance plans, begin with an honest assessment of your medical requirements.

Questions You Should Ask Yourself

- Do I need individual or family health insurance?

- Do I have any pre-existing medical conditions?

- How often do I visit doctors or specialists?

- Do I take prescription medications regularly?

- Am I planning major medical events such as pregnancy or surgery?

Your answers will help determine whether you need comprehensive coverage or a more basic cost-effective plan.

Step 2: Understand the Types of Health Insurance Plans

Health insurance structures vary significantly, and understanding them is critical when choosing the best option.

- HMO: Lower premiums with a limited provider network

- PPO: Greater flexibility but higher premiums

- EPO: No out-of-network coverage except emergencies

- HDHP: Lower premiums with higher deductibles

In Tier-1 countries, PPO and HDHP plans are especially popular due to flexibility and potential tax advantages.

Step 3: Compare Coverage Benefits Carefully

Not all plans provide the same benefits. Always review coverage details thoroughly.

Essential Coverage to Look For

- Hospitalization and emergency care

- Outpatient consultations

- Prescription drug coverage

- Mental health and therapy services

- Maternity and newborn care

- Preventive health checkups

Plans with broader protection may have higher premiums but typically provide better long-term financial value.

Step 4: Premium vs Deductible – Finding the Right Balance

| Factor | Low Premium Plan | High Premium Plan |

|---|---|---|

| Monthly Cost | Lower | Higher |

| Deductible | High | Low |

| Out-of-Pocket Cost | Higher during claims | Lower during claims |

| Best For | Young and healthy individuals | Families or chronic conditions |

The ideal balance depends on how frequently you expect to use healthcare services.

Step 5: Check Provider Network and Hospital Access

Always confirm whether your preferred hospitals, doctors, and specialists are included in the insurer’s network.

- Higher co-payments for out-of-network treatment

- Lower reimbursement rates

- Possible claim rejections

Network coverage is one of the most important cost factors in countries like the US and Canada.

Step 6: Review Co-Pays, Co-Insurance, and Out-of-Pocket Limits

Beyond premiums and deductibles, pay attention to hidden expenses:

- Co-pay: Fixed payment per medical visit

- Co-insurance: Percentage of treatment cost you must pay

- Out-of-pocket maximum: Annual spending limit before full coverage begins

Plans with lower out-of-pocket limits provide stronger financial protection in emergencies.

Step 7: Evaluate Add-On Benefits and Riders

Modern 2026 health insurance plans may include valuable optional benefits:

- Critical illness coverage

- Accidental disability protection

- Global emergency medical coverage

- Telemedicine and virtual consultations

These add-ons slightly increase premiums but can significantly enhance overall protection.

Step 8: Compare Health Insurance Providers

Never select a policy without researching the insurer carefully.

- Claim settlement ratio

- Customer reviews and satisfaction ratings

- Financial strength and stability

- Quality of customer support

Leading insurers in Tier-1 countries invest heavily in digital claims processing and faster reimbursements.

Step 9: Consider Tax Benefits and Employer Contributions

Health insurance premiums often provide financial advantages:

- Tax deductions for self-employed individuals

- Employer-sponsored premium contributions

- Higher tax efficiency with family plans

Always include tax savings when evaluating total plan cost.

Common Mistakes to Avoid

- Buying insufficient coverage to save money

- Ignoring exclusions and waiting periods

- Failing to disclose pre-existing conditions

- Skipping annual policy reviews

Expert Tips for Choosing the Best Plan in 2026

- Think long-term rather than yearly costs

- Select higher coverage in high-inflation healthcare markets

- Review your policy every year

- Maintain emergency savings alongside insurance

Final Verdict: Making the Right Choice

The best health insurance plan balances affordability, coverage depth, and provider flexibility.

- Young and healthy: Consider an HDHP with preventive care benefits.

- Families or medical needs: Choose comprehensive coverage with lower deductibles.

In 2026, smart health insurance planning is not optional—it is essential. Making an informed decision today protects both your health and your financial future.